I recently spent some time looking at CIPA data and wrote a few articles on my blog pertaining to these camera industry statistics. I thought Photography Life readers may find some of the data of interest. What follows are a few thoughts about the camera market, based on my interpretation of CIPA data. It should be noted that data is simply data and two people can look at the same information and arrive at differing interpretations. For folks who find the data of interest you can pop over to my blog to read a bit more. If you want to see the actual data reports I would encourage you to visit the CIPA website and access the data directly…then put on a pot of coffee, grab a calculator or open up Excel on your computer…and have some fun!

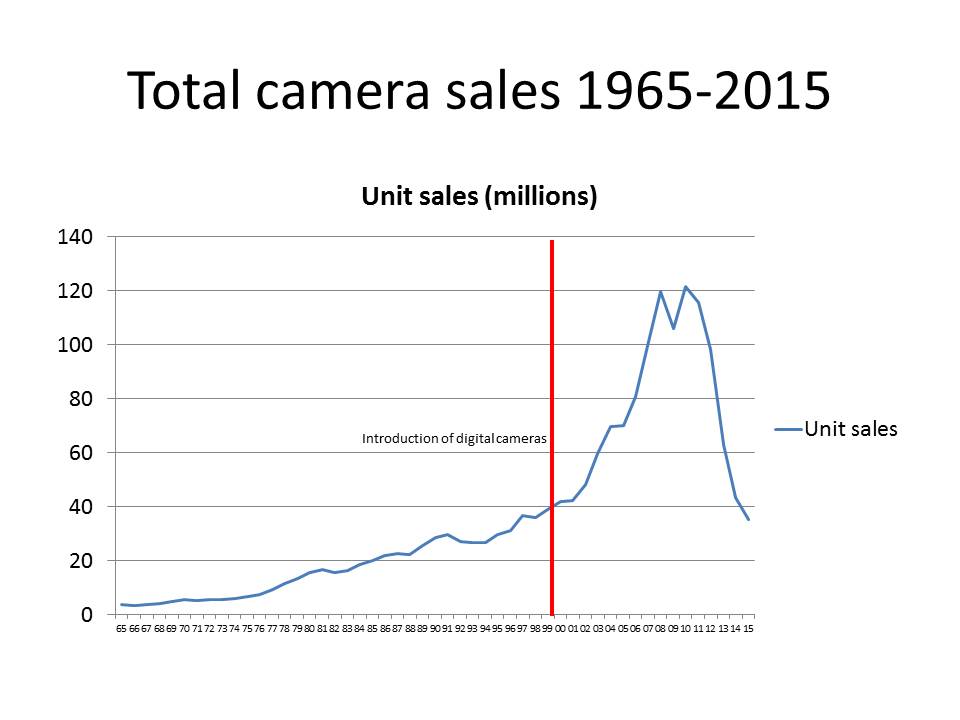

If we look at camera sales from a historical perspective we can see steady growth from the mid 1970’s through to 2001. When digital cameras were first introduced in the market it took about three years for them to really gain traction, then unit sales rose dramatically.

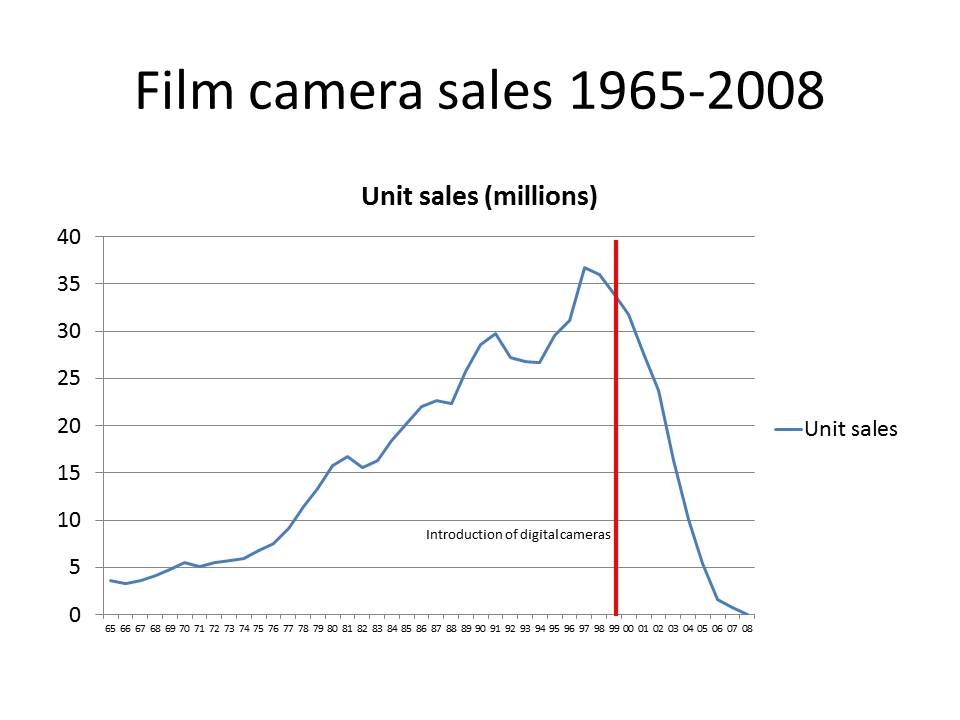

The chart above shows how quickly digital photography was adopted by the camera market. By 2008 the film camera market was basically dead.

Whenever a new technology like digital photography enters a market there are winners and losers. The first casualty was film cameras being supplanted by digital cameras.

The first cellphone with a camera was introduced in the South Korean market by Samsung in June 2000. That was followed by the first phone with a camera being sold in the United States in November 2002. Consumers loved the convenience and by the end of 2003 over 80 million of these new phones were sold worldwide. By 2011 the sales of cellphones reached into the hundreds of millions annually.

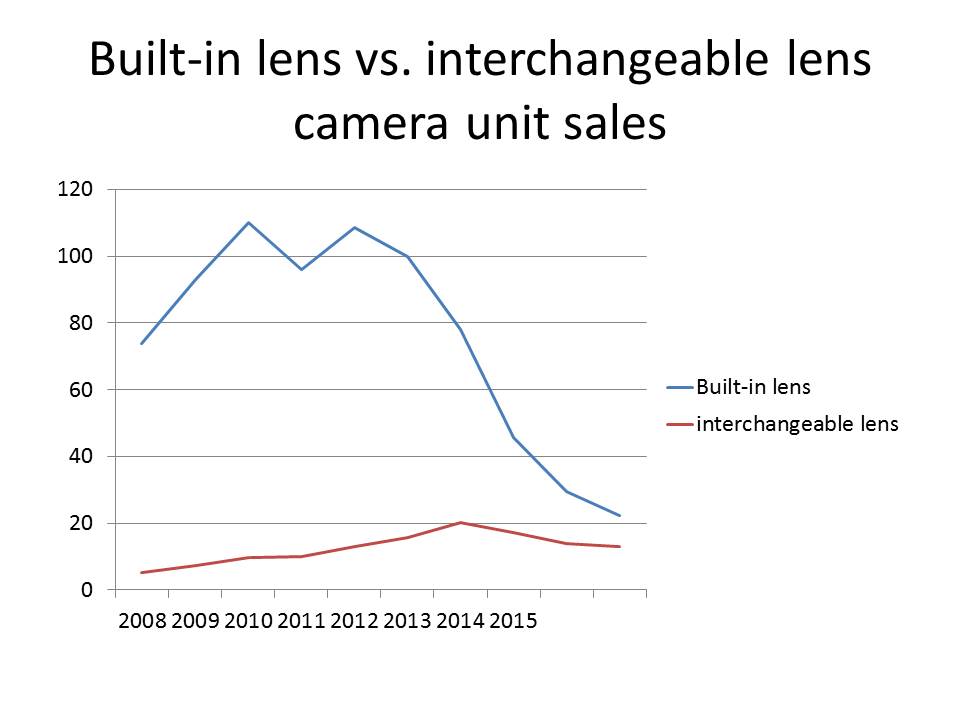

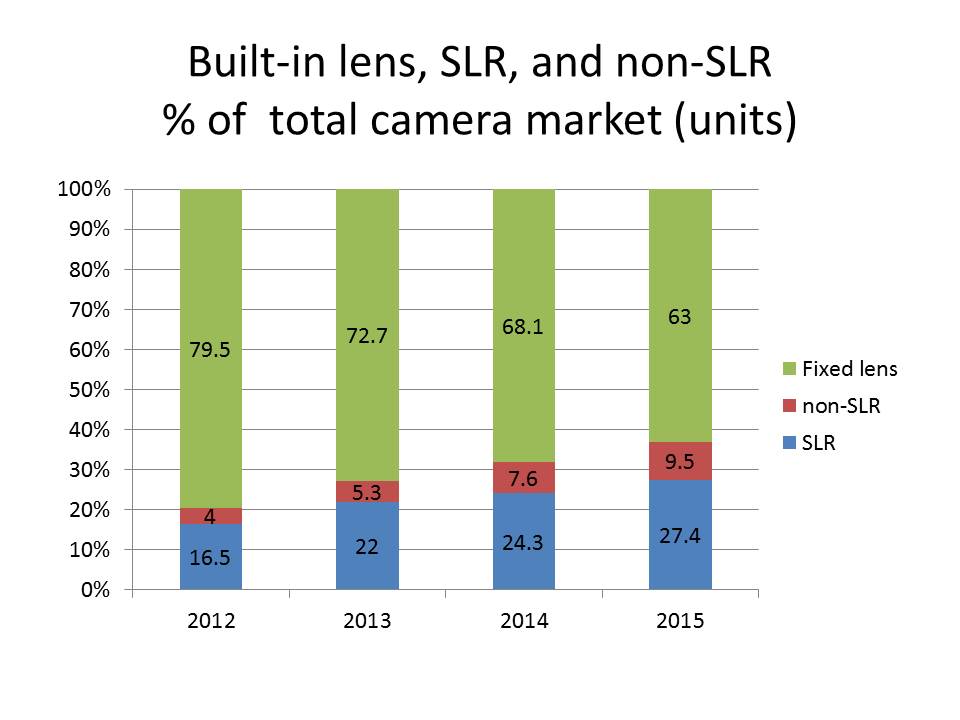

As you can see in the graph above the built-in lens camera market has dramatically fallen with the impact of the camera phone. But, there are also winners.

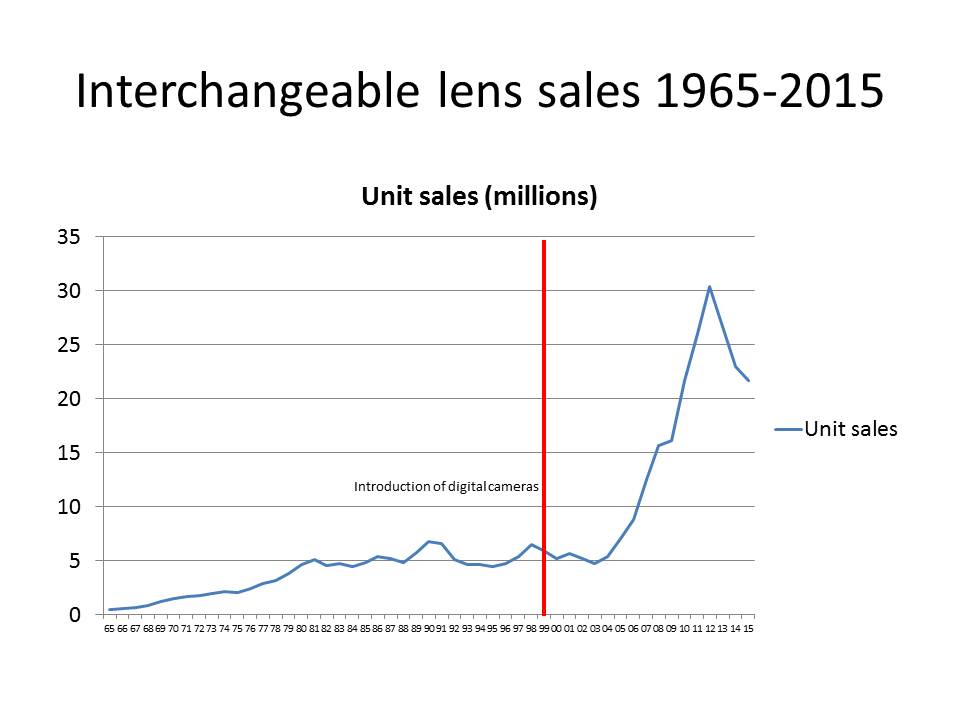

The sale of interchangeable lenses has increased dramatically as people needed to convert their gear to digital or chose to upgrade it to newer technology. While the unit sales of interchangeable lenses has softened since they hit their peak in 2012, as of the end of 2015 they are still more than triple the high water mark reached in 1997 in the film camera days.

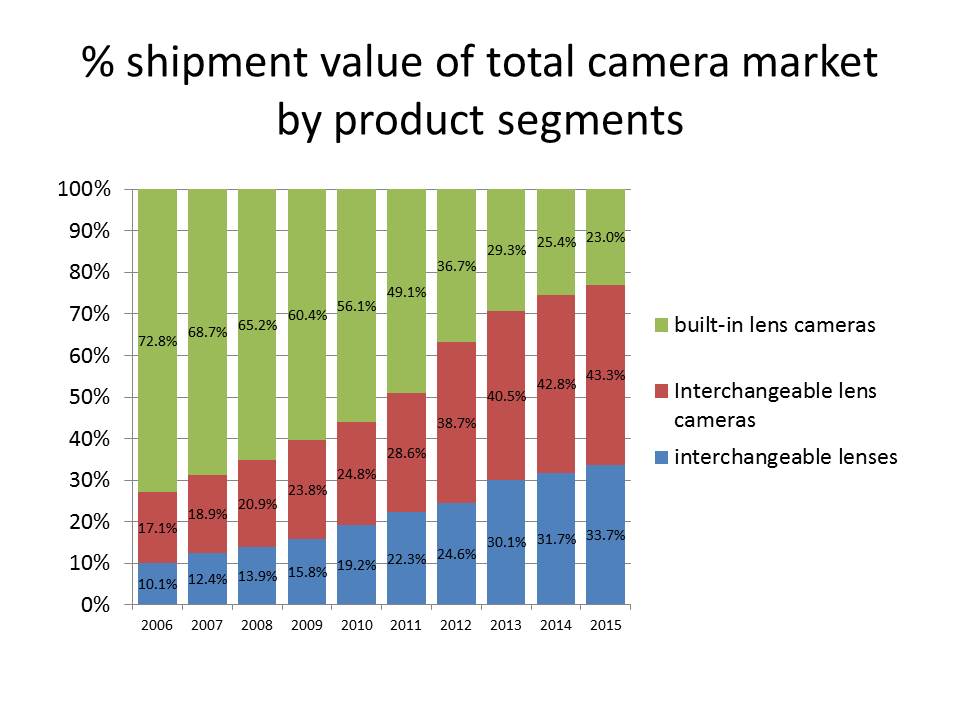

The above graphic shows the impact of the shift in units of various product segments in the camera market have impacted overall segment value. The built-in lens camera segment which used to generate 72.8% of overall shipment value in 2006 has collapsed to 23% in 2015 and now is the smallest segment. CIPA is forecasting further declines in the built-in lens camera market.

The above graphic shows the impact of the shift in units of various product segments in the camera market have impacted overall segment value. The built-in lens camera segment which used to generate 72.8% of overall shipment value in 2006 has collapsed to 23% in 2015 and now is the smallest segment. CIPA is forecasting further declines in the built-in lens camera market.

During the past few years we have seen camera manufacturers introduce higher content and more premium built-in lens cameras. Strategically this helps distance built-in lens cameras from camera phone capability, as well as generate more per unit revenue as overall unit sales continue to decline. The importance of the interchangeable lens camera segment and interchangeable lens segment have both increased in shipment value.

As the sales of built-in lens cameras declined the camera manufacturers shifted their research and development efforts away from this segment and put more focus on interchangeable lenses and interchangeable lens cameras.

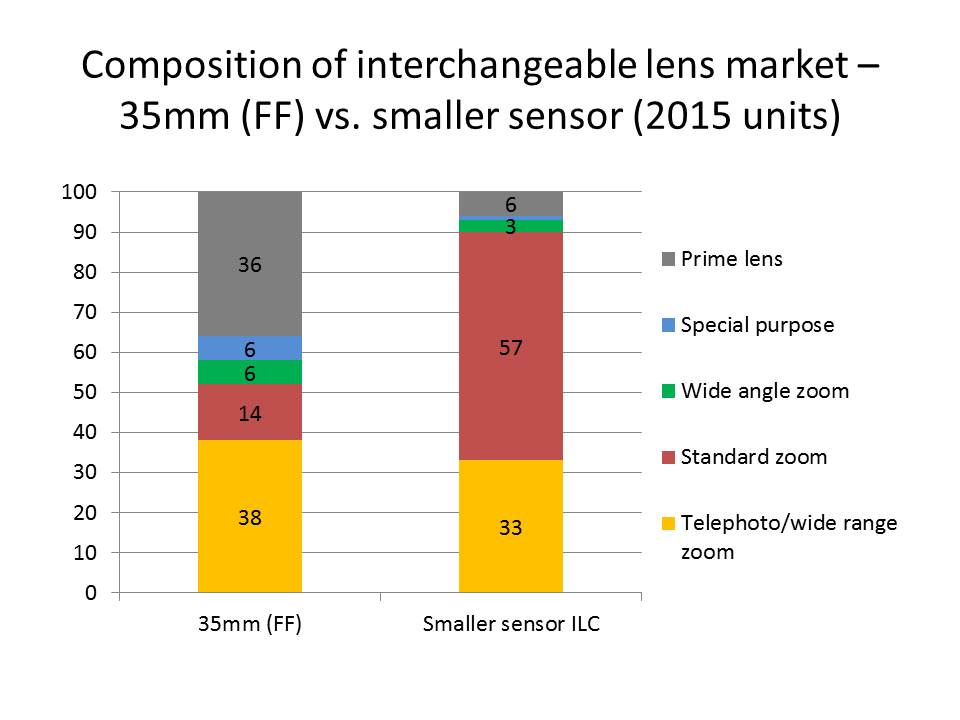

If we examine 2015 CIPA data regarding the composition of the interchangeable lens market we see a significant difference between the 35mm (full frame) market and the ‘less than 35mm’ market. Only 6% of the lens units sales in the smaller sensor market are prime lenses. This compares with 36% in the 35mm (full frame) market. Sales of zoom lenses constitute 93% of interchangeable lens sales in the smaller sensor market compared to 58% in the 35mm (full frame) market. Much of this could be the potential impact of more camera/lens kits being sold to the buyers of smaller sensor cameras. Another factor could be APS-C owners buying full frame lenses and using them on their cropped sensor gear.

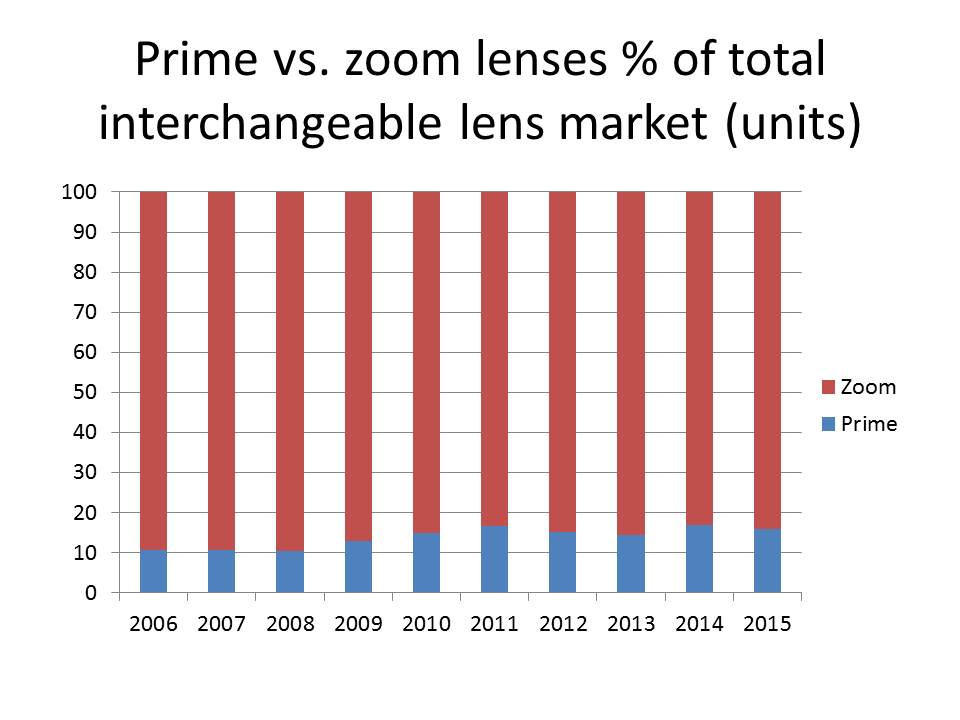

When we examine the global interchangeable lens market regardless of camera sensor size we can still see the dominance of zoom lenses which outsell primes by a ratio of 5.6:1. Approximately 85% of all interchangeable lenses sold globally are zooms. As various segments like the M4/3 and CX markets mature it will be interesting to see if there is any increased penetration of prime lenses. Next, let’s have a look at the impact of non-SLR (mirror-less) cameras.

In terms of unit sales we can see that from 2012 through to 2015 the market share of non-SLR (mirror-less) cameras has more than doubled from 4% to 9.5%. Built-in lens cameras still generate the lion’s share of the market’s unit sales but now constitute less than 2/3 of overall volume.

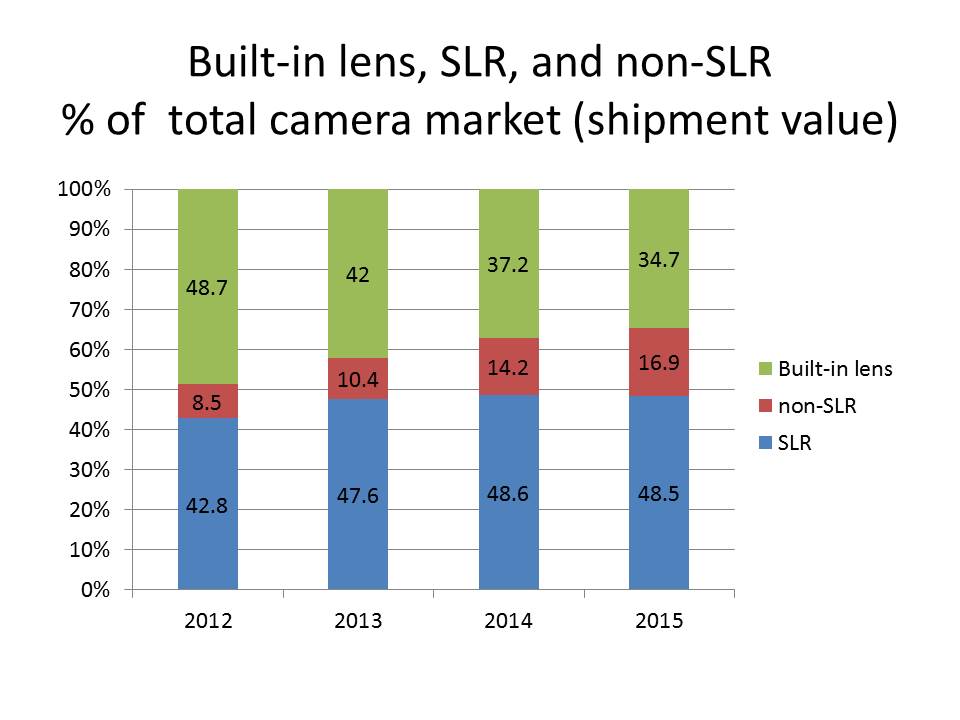

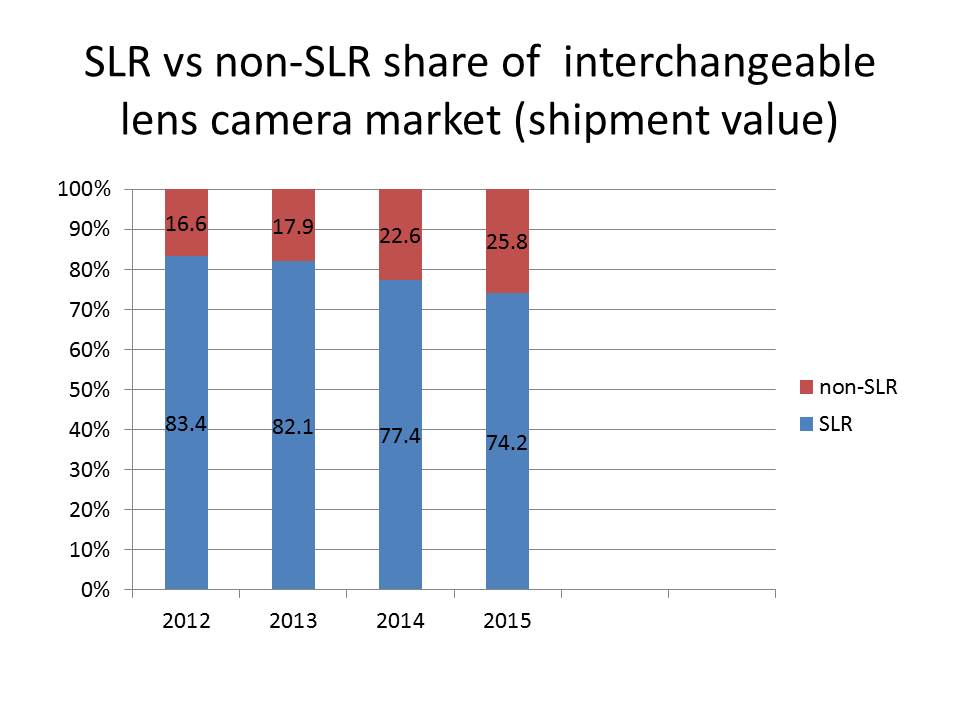

In terms of shipment value the interchangeable lens camera market has been growing in importance with SLR’s holding just under 50% of overall shipment value and non-SLR’s (mirror-less) almost doubling in value from 8.5% in 2012 to 16.9% in 2015.

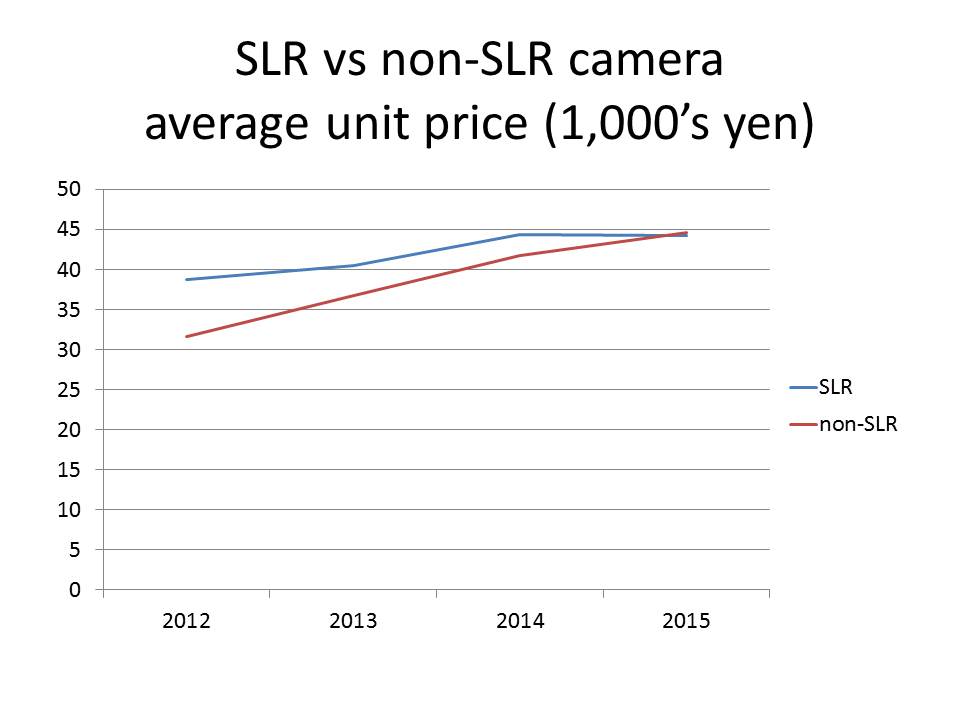

The per unit shipment value of a non-SLR (mirror-less) camera has risen over time and now is slightly higher than an SLR camera. We are likely seeing the impact of Sony 35mm (full frame) bodies and higher end M4/3 bodies from brands like Olympus, Panasonic and Fujifilm.

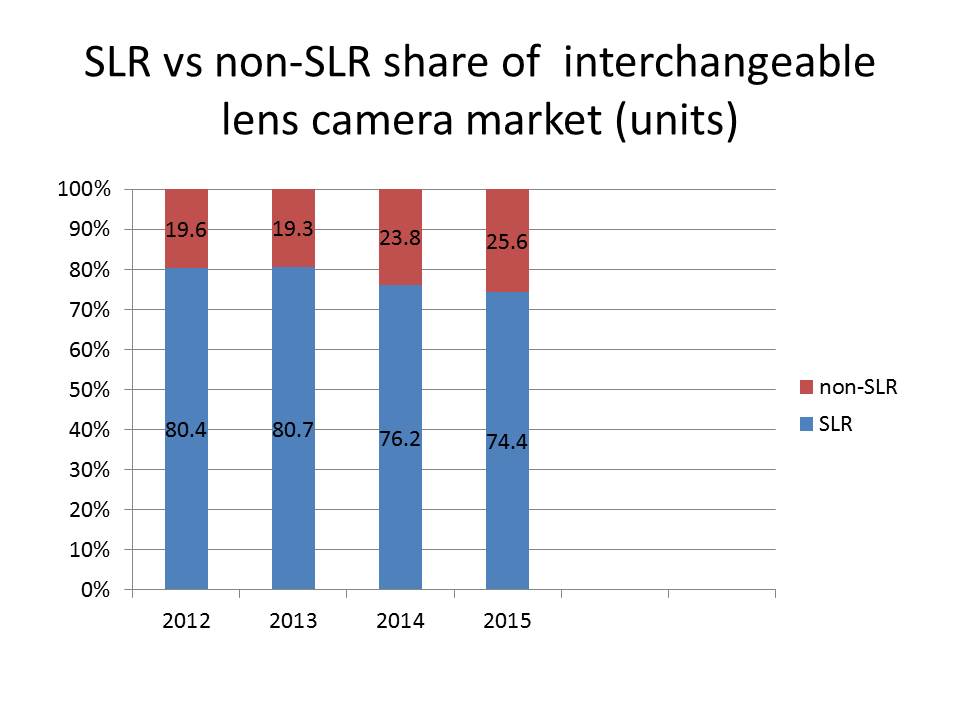

When we examine just the interchangeable lens camera market we can see that non-SLR’s (mirror-less) now account for over 1/4 of unit sales globally. It should be noted that the adoption rate of non-SLR (mirror-less) varies considerably around the globe with the Americas having the lowest rate.

The share of shipment value of non-SLR’s (mirror-less) has also grown and now stands at 25.8% of the interchangeable lens camera market value. If this trend continues at its current pace it would take about 5 years for the shipment value of non-SLR’s to overtake SLR’s in market value and will likely represent about 1/3 of market value by the end of 2017. If Canon and Nikon do not enter the non-SLR (mirror-less) interchangeable camera market with a good complement of APS-C and/or full frame cameras by the end 2017 they will likely miss an important strategic window of opportunity.

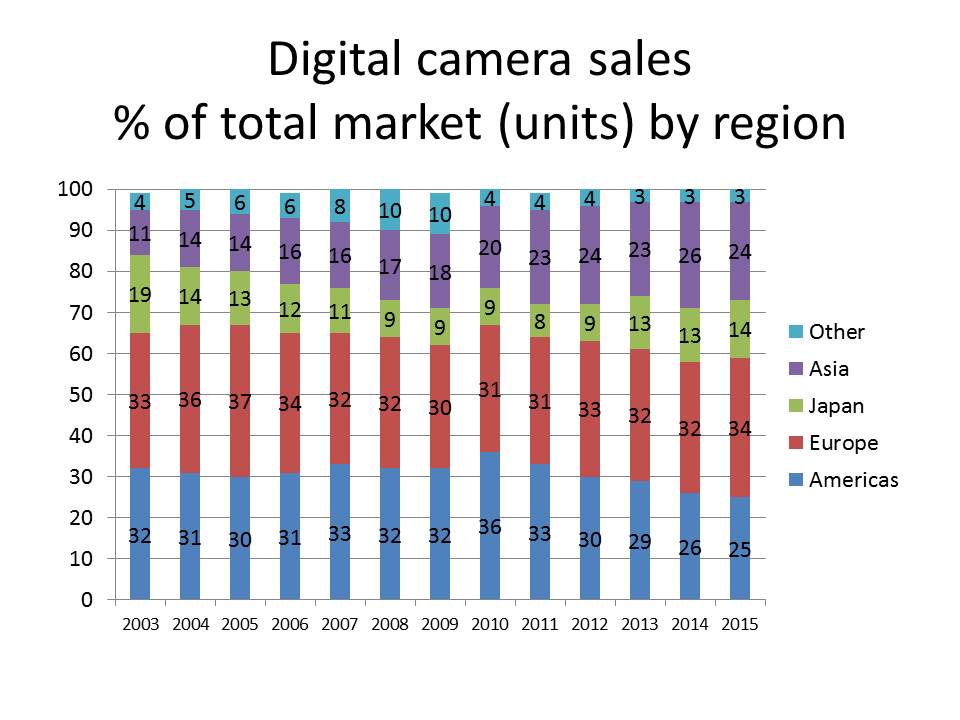

We can also see that the sales of digital cameras to various regions around the world has shifted over time with Europe being the largest digital camera market at about 34% of worldwide volume. This is followed by the Americas at 25% and closely followed by Asia at 24%. Japan is currently about 14% of worldwide digital camera sales.

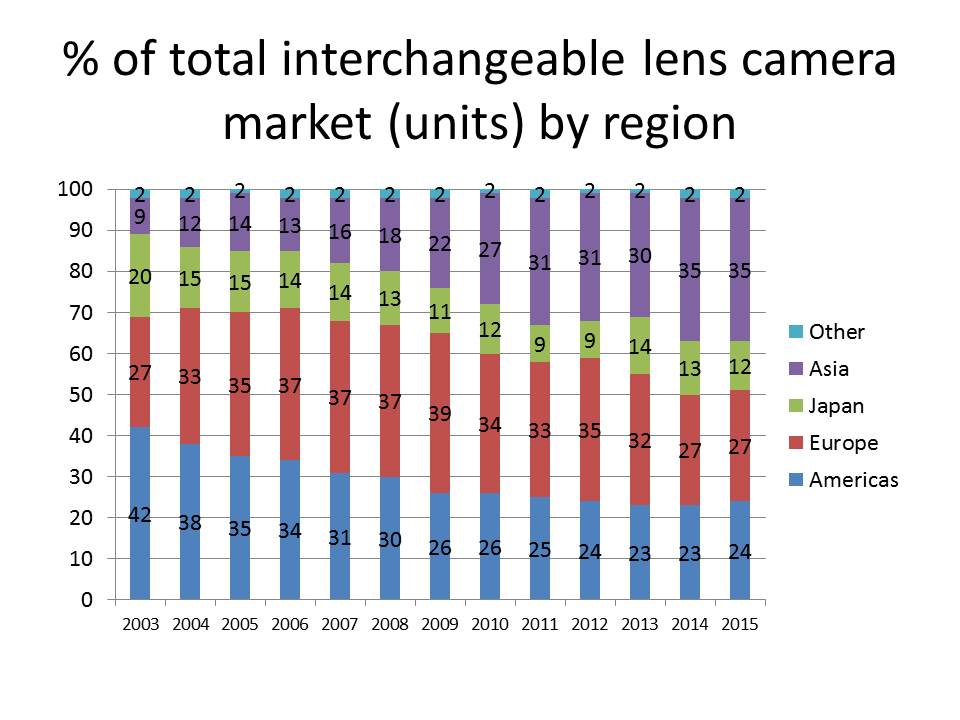

When we look at the sales of interchangeable lens cameras the data tells us a different story with the Asian market being the largest at 35% of global unit volume. This is followed by Europe at 27% and then the Americas at 24%. Japan represents about 12% of the global interchangeable lens camera market.

As consumers we sometimes scratch our heads when new products are introduced and we wonder what a particular manufacturer was thinking. It is always good to remember that many products like cameras are developed with a global market perspective and sometimes the needs of consumers in one part of the globe may overshadow the needs of smaller markets.

These are just a few quick highlights of the most recent data published by CIPA. If you’d like to see more please drop by my blog or visit the CIPA website directly. I also have my interpretation of the Nikon DL/Nikon 1 impact debate posted online.

Article and all graphics are Copyright Thomas Stirr. All rights reserved. No use, adaptation or duplication of any kind is allowed without written consent. This article was written specifically for use by Photography Life. If you see this article reproduced anywhere else it is an unauthorized and illegal use.

Got the CIPA data. Thanks!

Hi – great article.

I’d like to re-use one of your graphs on my blog – is that okay?

Will there a come a time when the mobile phone camera users will get fed up with their tiny lousy images and start buying DSLRs or mirrorless? When it happens the graphs will start moving up again. People will someday start upgrading their toys.

Thanks for sharing.

The DSLR is not dying. It is more likely that most people that want one now have one that meets their needs … even if it is 10 or 15 years old. The market is saturated. Makers are relying on people “upgrading” to newer and better technology, but when they have not even reached the limits of their “old” technology cameras, why would they? Technical obsolescence is not working. Most people are too sensible to jump onto the upgrade cycle, despite all the “encouragement” they get from the Internet.

Hi Tom,

Nicely written and presented assessment.

Ross

Thanks for the positive comment Ross!

Tom

Humans are curious creatures.

Once the fashion grows old we resume our regular lives until the next fashion.

Articles and graphs point to our silliness.

Good stuff on this post especially in the comments section!

Would be nice to have that kind of analysis again soon since this is about to be a year old.

I’ve landed here while looking for articles on the new established camera format, the Large Sensor Compacts and after reading you guys article on Nikon DLs announcement I clicked on the POINT AND SHOT tag which showed me this article as being the last one with this tag on it. Nothing since then!

Have you guys talked about the Large Sensor Compacts in me depth? Have you used a different tag on the blog than POINT AND SHOOT?

I used to have lessons on a Zenit 12XP paired with a Helios 58mm f2, when the digital era came was inevitable to swap for a point and shoot since I’ve never been a professional photographer rather an enthusiast. Things were very bulky for me to even consider a DSLR but when the Meireles Mirrorless cameras started to show I followed carefully the topic until Fuji showed what they’re here for and today I’m back on full composition mode photography with my Fuji X system.

I’ve recently became a father and at home or in situations where I know I’m going to take some shots, my Fuji is certainly on me. But I’ve noticed that I haven’t taken the camera out with me every day and have even left it home on a short weekend trip due to traveling lightweight.

Of course we both have current mobile phones with great cameras but after shooting my Fuji X is a bit hard to be happy with my phone camera sometimes… I already knew about Fuji X100 but what bothers me the most on mobile cameras is the fixed prime lens so the X100 wouldn’t suit my needs.

So I’ve started looking for what the market would offer for people like me in terms of an all in one solution camera that’s at the same time compact enough to take anywhere and good enough that I would care to take anywhere instead of just shooting with my phone.

That’s when I stumbled across this whole new world of 1″ Sensor Compact Cameras! I’ve found Nikon 1 and even the Micro Four Thirds not very interesting in terms of the lens selection, never a fast zoom and really one or two fast primes and never really grabbed my attention. All of a sudden there’s 1″, m4/3 and even 1.5″ sensor cameras with fast zoom lens! I was mesmerized to find out about it!

Following up on this article I would love to see how this new niche compares to the Smaller Sensor and Mirrorless. As someone stated on the comments, Video turned out to be a big USP with these cameras featuring 4k paired with tilt screen to record a vlog for their YouTube channel… Teenagers won’t go anywhere, therefore, YouTube is not going anywhere so as long as these companies are finding the new market they’ll be fine! And after all selling 100 cameras at $200 is pretty much the same of selling 20 at $1,000 isn’t it? Crappy Cheap point and shoot days are definitely over.

And Fuji now reinvented the wheel with a bigger sensor than Full Frame so how’s that for innovation in consumer products? Is there a market for that? We’ll find out soon right?

For now I would love to decide which Large Sensor Compact I’ll take home. I don’t know if you write reviews and comparisons for the website Tom and if not I would really appreciate if you could pass this message to the right person.

There’s a gap on in-depth reviews of these Large Sensor Compacts targeted to the enthusiast/amateur photographer. Most reviews are talking about Movie quality targeted to Vloggers.

Would be good for instance to cover how these cameras are handling Depth of Field, Bokeh rendering and low light photography with these bigger sensor and fast lenses even when compared to their bigger siblings the 1″ and m4/3 Mirrorless Cameras.

I’m very curious to see especially how the Canon G1X Mark II (with its 1.5″ sensor and longer focal length lens), the Panasonic Lumix LX100 (with its m4/3 sensor) and both the Canon G7X Mark II and Panasonic Lumix LX10 compare against each other on this DOF/Bokeh/Low Light fight. Been trying to decide between them but every one of them has an aspect that I would love to have and is been just too hard…

Plus the first two are probably due to an upgrade but neither companies are really talking about it… would be really disappointing to buy one of them just to see the dream one being released right after :(

Anyway, sorry for super long comment, was a bit carried away with the whole thing and possibilities!

Cheers from Down Under

Gus

Hi Gus,

Thanks for taking a considerable amount of time to share your perspectives! As far as an update to the camera statistics go I normally put something together once the year-end number from CIPA are available. That should be within the next month or so.

As far as how information on Photography Life is organized that’s really Nasim’s call as the owner of the site. Doing gear reviews is not something that I personally do very often. The ones I do are usually limited to gear that I own and use. I have requested review samples of the Nikon DL from Nikon Canada but I have no idea when, or if, I will be able to get access to that particular product line. If I am able to secure some review samples I will be writing some articles on my own blog, and may put a summary article together for Photography Life, assuming that no one else on the team does that before I have access to the review cameras.

As far as camera comparisons and other technically oriented articles go, Nasim and the other talented folks here at Photography Life are much better informed and equipped to do that type of posting. At this point I really don’t have any interest in owning or using a fixed lens camera so I won’t personally by dedicating any of my time to comparison type articles. Other than some potential articles on the Nikon DL series I have nothing else planned.

Tom

Hey Thomas,

I had a quick question you guys may be able to help me with. Im a recent college grad looking to do some part time photography and build my portfolio. I have been looking for a good camera with my graduation money, well part of it anyway. I was looking around the 1,000 to 1,500$ range. Anyway, I have read lots of reviews ect about different cameras and have taken a liking to the Canon EOS 5D Mark III It’s a lot more then my price range new but used i could possibly buy one. Or this Sony a7R II which i saw on this list www.bestcamerahq.com/cgi-s…edpage.cgi Do any of you have any experience with either of these or could recommend something that meet the above criteria?

Thanks for the help!

Hi Adam,

I don’t personally have any experience shooting with either Canon or Sony so I am unable to comment specifically on either of the two cameras you noted. I’d suggest that before leaping into buying any camera gear, especially based on some rating on the internet, that you determine what type of photography you will be doing. Consider what lenses you may need to capture various types of images and then start to plan out an overall system approach to your purchase. It is very likely that you’ll end up spending more money on lenses than a camera body (in the mid to long term anyway) so it is always wise to really think about what kind of camera system you’ll need. Both of the cameras you noted are full frame models which are likely overkill for someone just starting out. There are plenty of cropped sensor and M4/3 cameras that would also represent great options for you, as well as some quite competent super-zoom models. If you do a search here on Photography Life you’ll likely find some good articles specifically on what to consider when buying camera gear.

Tom

Let’s see. We have the Apple iPhone that comes out “new” every year. We have digital cameras that change every 6 months.

We have buyers who can’t wait to own the newest camera so their photos will be better. Cell phone photos filling the airwaves.

Can any of you remember finally getting a Nikon F? The ultimate camera that would last about 10+ years. The only thing then that changed was inexpensive film! What a different time.

My only point (as a digital photographer): Can we get sucked into this digital camera stuff to the point where we forget why we’re taking photos? Don’t laugh.

Hi Peter, you are absolutely right, to a point.

Oddly enough I was showing the family some old wedding and family shots on the computer an hour ago, great fun, but during that, I was zooming in on faces and it is remarkable how much better my images shot on my last three cameras are, compared to what I thought was a pretty good bridge camera five years ago.

By better, I mean in all the usual ways, sharpness, good focus, good exposure, lack of CA and all the other issues a lesser camera and lens offered.

I would say it is fair to say that once I got my D5100 the images lacked for nothing, other than selective cropping, or big enlargements where the resolution began to let the image down.

My current D5500 certainly does everything I care to throw at it, and to be perfectly honest with you, the change of model does not come without a level of pain. Although it is a similar interface, it does require a degree of re-educating in order to be using the camera at it’s best.

Then there is the need to upgrade other things – my last body upgrade forced a new computer, and a photoshop and DXO Optics Pro upgrade along with it!

I think, to the competent photographer, we have already ‘hit the plateau’ where image improvements can only come from better use of technique, rather than any kind of upgrading. In fact, I cannot be alone in this thinking, maybe that too is having an effect on sales of cameras. I certainly will not be upgrading again, now I know how to set up and use my camera in pretty much any situation.

I have benefited from all of my upgrades over the past five years or so, but I have to acknowledge that I have reached the point where I would be foolish to change anything now. I have a great macro lens, a nice everyday lens, and enjoy a superwide zoom and a very useful telephoto zoom when the occasion demands. Similarly I have a prime 50mm Nikkor for those low light moments, but that is rarely on the camera. Maybe now my upgrading and constant striving for ‘that camera’ or ‘that lens’ will cease, and allow me to enjoy the creative side of this far more from here on in.

You made a great observation.

NIkon F? Last 10 years. NO! Most of them will still be intact and capable of taking photos when all of us are long gone.